Meter

Quarterly Results Intelligence

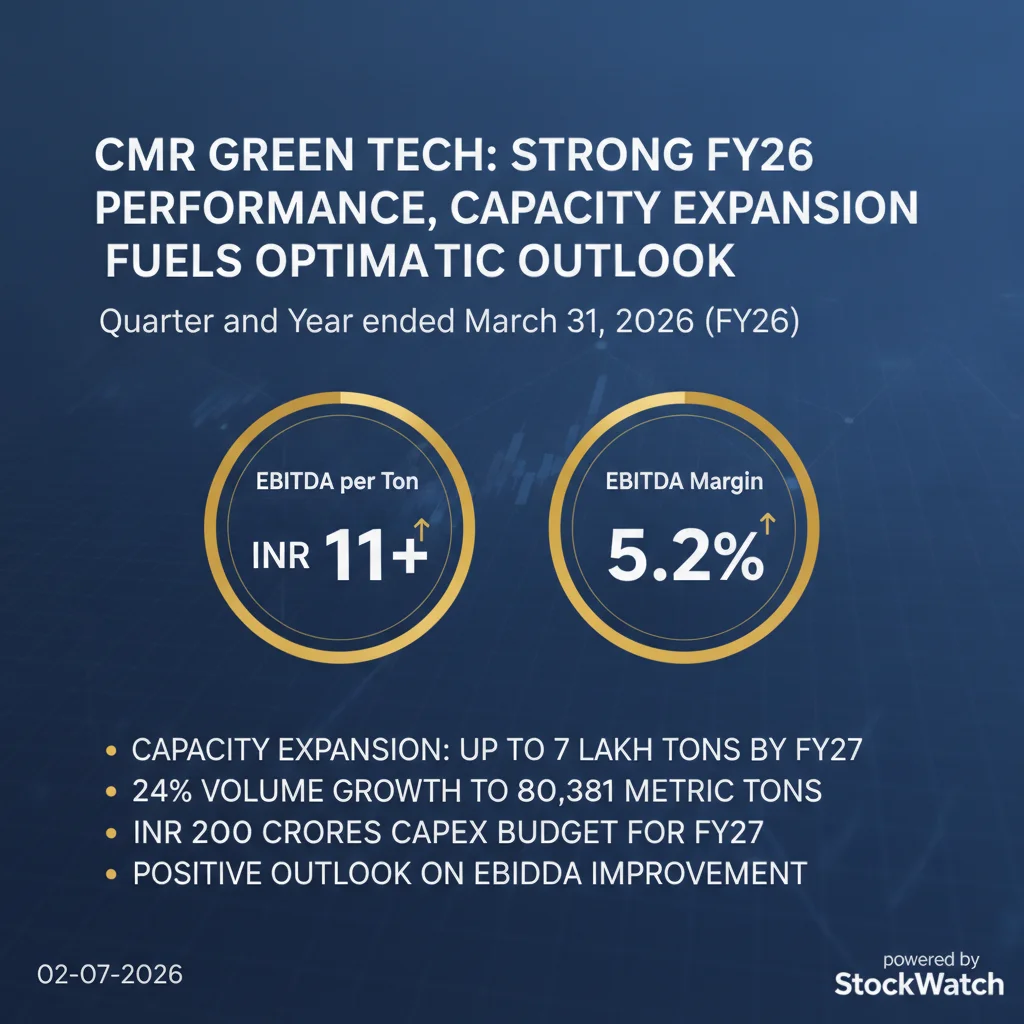

CMR Green Technologies Ltd

Management Guidance

Management provided optimistic guidance for continued growth, expecting similar volume growth rates in FY27 as experienced in FY26. They anticipate further improvements in EBITDA per ton through ongoing technological advancements, economies of scale, and the development of new alloys. Strategic capacity expansions in both aluminum and non-aluminum segments are underway, with a projected total capacity of 7 lakh tons by FY27. The company aims to maintain profitability through robust risk management and hedging strategies, even amidst commodity price volatility, and is well-positioned to capitalize on the increasing demand for recycled materials driven by industry trends and upcoming EPR mandates.

P/L Statement (in crores)

Press Releases

Earnings Call Recordings

Positive Outlook

CMR Green Tech: Strong FY26 Performance, Capacity Expansion Fuels Optimistic Outlook

CMR Green Technologies Ltd · CMRGREEN

Management Guidance

Management provided optimistic guidance for continued growth, expecting similar volume growth rates in FY27 as experienced in FY26. They anticipate further improvements in EBITDA per ton through ongoing technological advancements, economies of scale, and the development of new alloys. Strategic capacity expansions in both aluminum and non-aluminum segments are underway, with a projected total capacity of 7 lakh tons by FY27. The company aims to maintain profitability through robust risk management and hedging strategies, even amidst commodity price volatility, and is well-positioned to capitalize on the increasing demand for recycled materials driven by industry trends and upcoming EPR mandates.

HPL Electric & Power: Dual Growth Engines Drive Optimistic Outlook

HPL Electric & Power Ltd · HPL

Management Guidance

Management is confident in HPL Electric's future growth, driven by its two-engine strategy of smart metering and the Consumer & Industrial (C&I) segment. The company expects to cross 1,000 crores in C&I revenue in FY27 and maintain strong growth momentum in both segments. Smart metering order book visibility remains strong, with continued execution expected. The focus is on quality growth, improved product mix, pricing discipline, and efficient working capital management. Calibrated capacity expansion and continued R&D investments are also key priorities. While margins in C&I were impacted by commodity price increases and a higher share of wires and cables, management anticipates margin recovery in the coming quarters due to easing inflation and price adjustments.

HealthX Platform Ltd: FY26 Growth, JITO Expansion, and Capital Efficiency Drive Optimism

Sastasundar Ventures Ltd · SASTASUNDR

Management Guidance

Management projects strong revenue growth, targeting ₹6,000 crores by FY30, with ₹4,000 crores from B2B Retailer Shakti and ₹2,000 crores from B2C SastaSundar App. They anticipate progressive improvement in EBITDA margins, aiming for 5% at scale, and maintaining industry-leading working capital efficiency. The company is investing in technology, automation, and platform capabilities to drive operating leverage and profitability. They expect JITO private label margins to range from 30% to 40% plus, with a focus on scaling this ecosystem. For FY27, Retailer Shakti is expected to see significant revenue growth, potentially reaching ~₹1,700 crores, with a targeted EBITDA margin of 1% for the entire financial year.

RACL Geartech: Milestone Revenue, Strong Growth, and Strategic EV/Premium Segments Drive Bullish Outlook

RACL Geartech Ltd · RACLGEAR

Management Guidance

Management provided a robust outlook, projecting continued growth with revenue expected to exceed 565 crores plus or minus 5% for FY27. The company is strategically investing in high-growth segments like electric vehicles and premium motorcycle applications, evidenced by new customer wins and ongoing project developments. While focused on sustainable growth, the company is confident in meeting its guidance and sees potential to surpass 1000 crores in revenue within the next three to five years, signaling a strong long-term expansion strategy.

Systematic Industries Pivots to High-Growth Sectors with Strong FY26 Results

Systematic Industries Ltd · SYSTEMATIC

Management Guidance

Systematic Industries is projecting significant growth driven by its strategic transition to 'New Age' segments like OPGW and OFC, which are expected to contribute substantially to profitability from FY27 onwards. The company has secured key EPC contracts and is poised to benefit from a substantial OPGW tender pipeline. Management plans to scale 'New Age' assets and maintain a net debt-free status, focusing on premium steel wire segments and increasing export contributions.

BEML: Strong Order Pipeline and Innovation Drive Positive Outlook

BEML LTD. · BEML

Management Guidance

Management provided a strong outlook, projecting an order book of ₹15,900 crores with an aim to add a similar amount in the current year, leading to a potential year-end order book of ₹24,000 crores. Revenue execution is expected to be more balanced across quarters, moving away from the historical Q4 skew. Guidance indicates a shift in revenue mix, with Rail & Metro and Defense expected to constitute 65-70% of the total revenue in the medium to long term, while Mining will form a baseline of 30-35%. Sustainable EBITDA margins are targeted at around 16%, with exports and high-end heavy earth moving machinery and commuter rail being key margin drivers. The company is investing significantly in R&D (targeting 7% of sales) and capacity expansion, particularly for rolling stock production, to meet future demand and leverage new product development, including electric vehicles and advanced rail technology.

Aegis Logistics: Breakout Year, Strong Growth, Ambitious Capex

AEGIS LOGISTICS LTD. · AEGISLOG

Management Guidance

Management expects FY27 to maintain the strong momentum seen in FY26, guided by a conservative philosophy of under-promising and over-delivering, targeting a 25% CAGR growth. A significant capital expenditure pipeline of approximately $5 billion through 2030 is planned, with a substantial portion to be deployed by 2028, focusing on both traditional energy infrastructure and emerging energy transition value chains. The company anticipates continued revenue growth driven by increasing volumes, particularly in the gas distribution segment, and expects to sustain EBITDA margins around INR7,000 per ton due to volume-driven procurement efficiencies.

Aegis Vopak: Strong Growth Trajectory Fuels Bullish Outlook with Ambitious Capex

Aegis Vopak Terminals Ltd · AEGISVOPAK

Management Guidance

Management provided a highly optimistic outlook, projecting a significant ramp-up in capital expenditure to USD5 billion by 2030, with a substantial portion expected in the latter half of this period. They anticipate continued year-on-year throughput growth of 30-40% and are strategically diversifying into ammonia and other emerging energy transition products, aiming to expand their port presence and explore inland infrastructure. Revenue is expected to be driven by capacity additions and a favorable product mix, with gas terminaling projected to become the dominant segment. While specific revenue guidance is not provided, the company emphasized strong revenue visibility through long-term take-or-pay agreements and a disciplined financial approach.

IFB Industries: Growth Momentum & Strategic Expansion in FY27

IFB INDUSTRIES LTD. · IFBIND

Management Guidance

Management anticipates continued strong revenue growth in home appliances, targeting over 20% for FY27, driven by market share gains and strategic product portfolio rationalization. The engineering division is projected to achieve 20-25% growth over the next 2-3 years, supported by new revenue streams and capacity expansion, with a target EBITDA margin of 17-18%. While cost optimization initiatives are ongoing, management acknowledges that the full impact of commodity and forex headwinds has not yet been entirely offset, but expects ongoing improvements. The company is also focusing on expanding its presence in newer categories like ACs and refrigerators, aiming for double-digit market share.

Srigee DLM: Expansion Fuels Optimistic Outlook, Polymos & ODM Key Growth Drivers

Srigee Dlm Ltd · SRIGEE

Management Guidance

Management projects strong growth for FY27, targeting INR 100 crores in turnover, with a confident outlook for INR 200-250 crores in FY28, and a peak potential of INR 350 crores at the new facility. Margin expansion is expected due to increased capacity, operational efficiencies, and the strategic development of the polymer compounding and ODM segments. The company is focused on expanding manufacturing capacity, strengthening ODM capabilities, and increasing its presence across high-growth end markets, with a commitment to building long-term customer relationships and creating sustainable value. Capital expenditure for the new facility is estimated at INR 25 crores, with funding from a combination of equity, debt, and asset sales.

Cautious Outlook

Avanti Feeds: Navigating Raw Material Costs Amidst Export Growth & New Ventures

AVANTI FEEDS LTD.-$ · AVANTI

Management Guidance

Management anticipates a challenging environment in FY27 due to steep increases in raw material costs, particularly fish meal and soya bean meal, potentially necessitating feed price hikes. However, they are optimistic about overall growth, projecting a 10-15% increase in revenue and profit, driven by improved capacity utilization in frozen products, expansion in value-added offerings, and the burgeoning pet care business. The company expects to stabilize feed prices through government representations and potential import permissions. Shrimp exports are projected to grow, with a favorable outlook in the US and Europe, alongside strategic expansion into new markets and product categories.

RMC Switchgears: Navigating Challenges, Focusing on Tech-Led Solutions for Future Growth

RMC Switchgears Ltd · RMC

Management Guidance

Management acknowledges FY26 was a year of progress with 26.4% revenue growth but lower-than-expected profitability due to product development investments, project execution delays, and input cost pressures. For FY27, the company expects to perform better than last year, incorporating buffers for unexpected issues, and a renewed focus on profitable, sustainable growth. Long-term, the company aims to evolve into a diversified electrical infrastructure and technology solutions provider, targeting a Rs. 5,000 crore revenue aspiration by 2030, driven by technology-led innovation and addressing key utility pain points.

HGS: Transformation to Intelligent Experiences Fuels Growth Amidst Media Business Challenges

HINDUJA GLOBAL SOLUTIONS LTD. · HGS

Management Guidance

Management expressed cautious optimism for the near term, citing ongoing macro uncertainties and client caution, but indicated steady improvements in growth and margins over time due to a high-quality pipeline, AI differentiation, and disciplined execution. The company is prioritizing sustainable, profitable growth with a focus on productivity, cost discipline, and capital efficiencies. For the long term, management sees a bright future as the company transitions into a technology services provider focused on intelligent experiences, supported by new platforms and strategic investments.

VTM Limited: Navigating Tariffs & Diversifying Markets for Resilient Growth

VTM LTD. · VTMLTD

Management Guidance

Management anticipates a 12-14% increase in top-line revenue for the current financial year, with efforts to improve profitability. They are exploring new markets like Japan, Europe, UK, and Australia to de-risk from US dependency. While FY25 EBITDA margins of 19% are considered exceptional and unlikely to be repeated, the company targets 10-11% EBITDA margins for the current year, aiming for potential 15%+ EBITDA margins in the long term through market diversification and product mix optimization. They foresee a run rate of 500-600 CR in revenue potential if conditions are favorable, with clarity on future strategy expected in the next two quarters.

Meta Infotech: Strategic Investments Drive FY26 'Investment Year', Optimism for 3-Year Growth

Meta Infotech Ltd · METAINFO

Management Guidance

Management has strategically positioned FY26 as an investment year, with significant investments in talent, geographical expansion, and technology partnerships. While FY26 saw reduced profitability due to these investments and unforeseen events like dollar fluctuations and the Imperva sale, the company is confident in its foundation. Looking ahead, Meta Infotech projects a 4x growth in Profit After Tax by FY29, driven by a sharpened focus on high-margin cybersecurity services, international market expansion, and leveraging new capabilities like AI security. Revenue recognition for large deals will be managed to provide better predictability, and the company aims to increase the contribution of services to total revenue significantly. The order book of INR506 crores provides strong visibility for the next three years.

GIC Re Navigates Competitive Market with Strong Capital, Focus on Disciplined Growth

General Insurance Corporation of India · GICRE

Management Guidance

Management expects FY27 to be a period of stabilizing yet competitive market conditions. They anticipate single-digit growth due to a soft pricing environment, prioritizing disciplined risk selection and prudent capital use over aggressive premium chasing. The company aims for a 1-2% year-on-year improvement in the combined ratio, with a specific target for more significant improvement in the international segment. Strategic focus remains on strengthening capital adequacy and maintaining financial stability through disciplined underwriting and portfolio optimization.

Tega Industries: Molycop Integration Underway, Solid FY27 Outlook, Consumables Stable

Tega Industries Ltd · TEGA

Management Guidance

Management provided guidance for a 5% year-on-year revenue growth in FY26, with an adjusted EBITDA margin of 22%. The company expects continued strong performance in the equipment business (25% growth) and mid-to-high single-digit growth for consumables, targeting a 15%+ long-term CAGR for consumables. For FY27, Tega expects around 15% growth on its non-Molycop business and a cautious 3% growth for Molycop, with a focus on integrating Molycop to unlock revenue and cost synergies. Capex for FY27 is projected around $55 million, including $25-30 million for the Chile plant, and maintenance capex for both Tega and Molycop, to be funded through internal accruals and borrowing. The long-term strategy includes reducing Molycop's debt to 3x leverage within 3-4 years and exploring non-core asset sales. The company expects the Chilean plant to commission by early Q3, with potential revenue booking by end of Q4 or early next year, subject to regulatory approvals.

NIS Management: Navigating Regulatory Changes, Focusing on Growth & Compliance

NIS Management Ltd · NISMGMT

Management Guidance

Management projects FY27 consolidated revenue growth of 12% to 15%, with a target to cross INR500 crores. They expect to deploy remaining IPO proceeds within two years. The company anticipates a strong pickup in the CCTV segment by year-end, driven by new tenders and AMC contracts, and sees significant opportunities in government and private sectors, emphasizing a balance between growth and operating cash flow. The new Labor Codes are seen as a long-term positive for formalization, potentially benefiting the company.

Ashapura Minechem: Strong FY26, Navigating Guinea Quotas for Future Growth

ASHAPURA MINECHEM LTD. · ASHAPURMIN

Management Guidance

Ashapura Minechem reported its best year ever in FY26, with a 105% revenue growth and significant profit margin expansion. For FY27, the company is targeting 10-12 million tons of bauxite volume from Guinea, with an estimated revenue of at least $700 million, and expects continued stable to good performance in its India business. Management anticipates improved net bauxite prices post the implementation of the Guinea quota system, although Q1 FY27 may remain challenging due to freight costs and geopolitical uncertainties. The company is focused on increasing port capacity to 27 million tons and has plans for iron ore beneficiation and bauxite washing plants, aiming for cost reduction and enhanced profitability over the medium to long term.

Radiant Cash Management: Navigating Subdued FY26, Focusing on Core Growth & Subsidiary Turnaround

Radiant Cash Management Services Ltd · RADIANTCMS

Management Guidance

Management expects to restore EBITDA margins to past healthier levels through rigorous focus on adding direct clients, increasing trust on dedicated cash vans, and empanelment of smaller banks. For FY27, consolidated revenue is targeted at INR5 billion with PAT margins between 11-12%. Both subsidiaries, Radiant Acemoney (fintech) and Radiant Valuable Logistics (RVL), are expected to achieve EBITDA breakeven in the first half of FY27, with Acemoney potentially reaching INR50-75 crores in revenue in two years. The core business is projected to grow at mid-teen rates in revenue for FY27, with a long-term PAT growth expectation in the mid-teens.